Hey everybody. This is Travis Konarik and today I’m going to give you a reason why you should not do your books from your bank statements. Business owners often use this as a crutch to save time and lower their back end expenses. In my experience, businesses that enter transactions this way typically cause problems that show up later, often at tax time. Today we are going to focus on sales documents and my goal is to give you some insight as to why this is bad, the problems it causes, and the method that we prefer.

Sales Documents

The first thing we need to discuss is where to get our sales records from. Sales are recorded in many different ways depending on your type of business. When we start with a new client, the sale is usually marked with an engagement agreement. If your business is a retail store front, sales will probably be recorded with receipts and reports from a register or point of sale. In the construction world, sales are often started when a contract is signed. When you purchase a car or buy a house, all the papers that you sign are part of their sales process. In the online world, the sale documents contain the same information even though the reports are on a different media and are accessed differently.

Get These To The Back Office

Have you ever stopped to think why all of this paperwork is important? It’s for your business records. Recording these documents gives you the paper trail for audits and legal purposes. We often see new service business owners fail here. They either do not document a sale at all or they do not get these reports to the person who is responsible for recording them. Missing these two steps can cause some of the largest headaches in your business. And I know what some of you are thinking, “Only a newbie could mess this up” or “My business has a point of sale. We have this covered.” Sometimes untrained employees cause problems here. They mean well, but don’t know how to enter the sale properly. They take the customer’s payment, hit no sale, and stick the money in the drawer. Many problems stem from sales that are not recorded properly or not at all. Any business that has ever had a sales tax audit knows this all to well. Calculating sales tax payments without the proper documentation will be very inaccurate. And if you happen to get a sales tax audit, messy, incomplete, or even worse, no records will make your life more painful than the audit alone. Another problem that starts here is accounts receivable tracking, also known as remembering who owes you money. It is too easy to track who owes how much money with a computer. It takes the guess work out of things.

Enter Sales Documents In QuickBooks As Invoices

Next I want to give you a quick run down of how to track this information in QuickBooks. In QuickBooks Online and QuickBooks Desktop this process should always start with the invoice screen. If you always enter this information on the same screen, you can greatly simplify your accounting process. Like many new things, this process may seem foreign when you first try it. Behind QuickBooks is the traditional accounting process. If accounting is not one of your strengths, don’t worry I will outline the process for this part of the framework.

QuickBooks expects three steps from you when you make a sale. Create an invoice, receive a payment, and then deposit the payment. As long as you remember that these three steps must exist for every sale you’ll be fine. QuickBooks makes your life easy by setting up a form that records each step in this process. If you want to record a sale, select Create Invoices. When you have received a payment, enter it in Receive payments. And once you have made your deposit, you can go to the Record Deposits screen and select the payments that you would like to deposit. It is very intuitive.

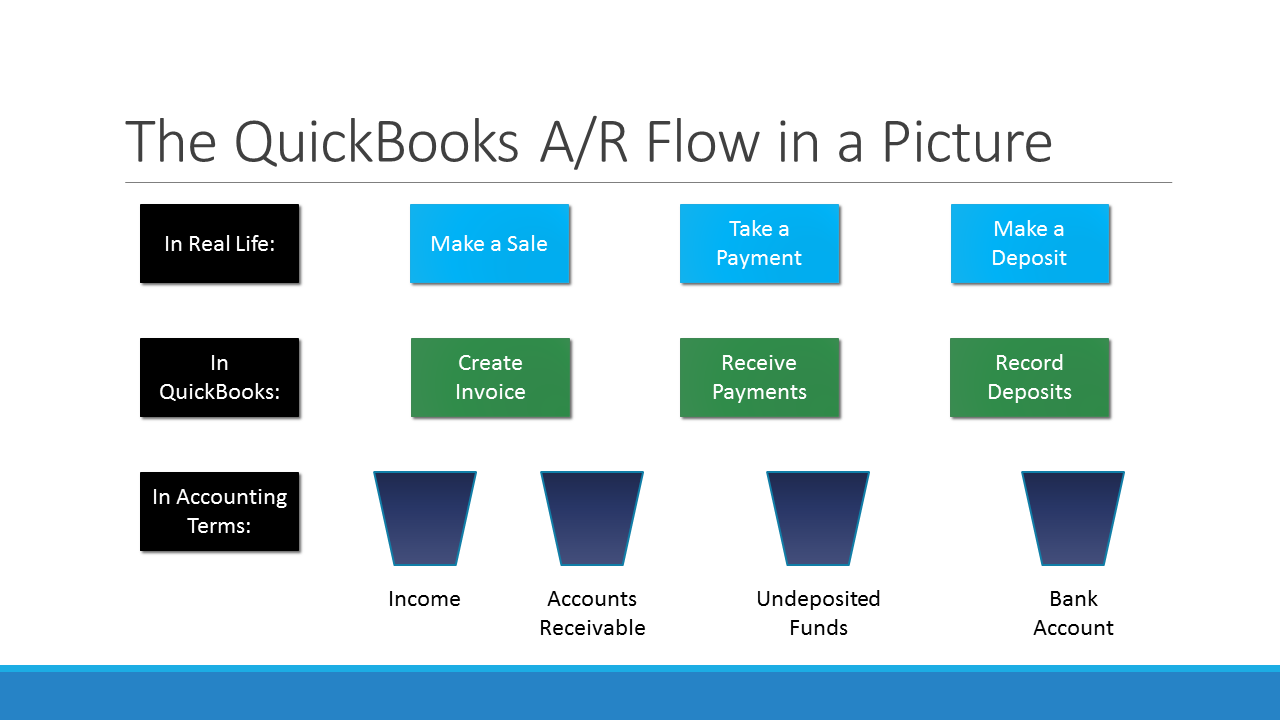

The QuickBooks A/R Flow

I just want to take a step back here and say that for most businesses we recommend entering all sales documents from this screen. It does not matter if you use an “invoice” in your sales process or not. Recording transactions in this manner will help you and your accountant understand some vital information regarding your sales, payments, and deposits.

Now that you understand where and when to enter your sales documents, I want to walk you through what is happening under the hood. This is often the source of confusion for many business owners we deal with.

I like to think of accounting as putting money in buckets. If you are familiar with accounting principles, you know that the common form of accounting is the double entry method. This just means that every transaction is recorded in two places, or in my terms affects the money in two buckets.

When you use the Create an Invoice screen to record a sale, QuickBooks places the sale amount into two buckets. For example, if you sold a 5 dollar widget, QuickBooks would enter 5 dollars into an income account and 5 dollars into an accounts receivable account.

After your customer pays you for the widget, you would enter a 5 dollar transaction into the Receive Payments screen. Behind the scenes, QuickBooks makes a transaction that affects the accounts receivable account and the undeposited funds account. Let’s look at a picture to help see the process.

This is the standard work flow for all sales transactions in QuickBooks

Here we can see the different layers and how they correspond. We have the sale which is entered from the Create Invoice screen. It affects the Income and Accounts Receivable buckets. Then we take payment from the customer. This step is entered on the Receive Payments screen. It affects the Accounts Receivable bucket and the Undeposited Funds bucket. The last step is to put the money in the bank. This step also corresponds to putting cash in a safe or having credit card funds deposited into your bank account directly. You record this step with the Record Deposits screen. The back end transaction affects the undeposited funds account and the final bank account that the money is deposited into.

The import things to note is that this process happens for every transaction you make in QuickBooks using this process. If your sales process is set up to take payments from your customer, this can easily be recorded using this process and QuickBooks can track it flawlessly. The other point of showing you this is so you notice that skipping any of these steps will cause the backend to have incorrect information. All reporting in QuickBooks comes from this backend information.

What Does This Do For Me?

At this point you might be wondering why any of this is important. To me, this process is part of a framework that simplifies the process for entering information into QuickBooks. Whenever I am setting up a new client, I always train them and their staff to enter sales in this manner. When I need to look at a businesses sales, I know exactly what to look for and where to look for it.

Another benefit to this process is that posting the sales as invoices allows us to review a business’s accounts receivable in reports. These reports can give us valuable information regarding who owes the company money, how much they own, and how long they have owed that money. Another great feature is that statements can be produced from a customer’s accounts receivable balance. These statements show them what they have paid for and what their outstanding balance is.

The last benefit to this method is that the bank account transactions in QuickBooks are clean. My goal when working on a set of books is for the bank account ledger in QuickBooks to match the bank statements as closely as possible. This makes reconciling the bank statement a breeze. It also aids in researching deposit origins when questions arise later on down the road.

What To Look Out For

Like all new processes, difficulties can arise until you master them. The most common place for error is when a sale is recorded, and the payment is later recorded as a deposit without first using the Receive Payments screen. The easiest way to fix this is to delete the deposit, enter the payment as received, and then re-enter the deposit. This problem can be eliminated by following this system’s steps in order: Create the Invoice, Receive the Payments, and then Record the Deposit.

Always Use Invoices To Track Sales Transactions

Implementing this method in your business will give you control of your business and help inform you about its financial position. I’ve seen businesses grow profits simply by realizing that some customers had missed their payments. Other businesses use this information to ensure they regularly follow up with accounts that are behind on payment. At the very least, this process will help your business become more organized. Each step towards organization is another step towards audit-proofing your business.

Go To www.InnovativeBookkeepers.com/Guides to sign up for our guides.

I use a number of simple, easy to follow processes like this one in my business. If you go to innovativebookkeepers.com and click on Tips, I have more short, informative posts with great information like this one. If you go to innovativebookkeepers.com/guides, you can also sign up for the guides that we send out. We send them out regularly and they will take a topic like this one, and give a deeper dive into the information. In these guides, I walk you through the screens and talk you through the information you need to enter. I always appreciate your feedback, so comments are always welcome.